Leander's location on the northwest edge of the Austin metro puts it directly in the path of severe Hill Country storms. If you've lived in Crystal Falls, Mason Hills, or any Leander neighborhood for more than a year, you've heard the warning sirens.

When hail, wind, or flash flooding damages your roof, the next 48 hours are critical. As Leander's trusted storm damage roofing contractor, we help families navigate insurance claims and emergency repairs.

This is your complete guide to protecting your home and getting the insurance coverage you deserve.

The First 24 Hours: Emergency Response Checklist

Immediate Actions (During/After Storm)

1. Stay Safe First

DO:

- Wait until storm passes completely

- Stay indoors until authorities say it's safe

- Monitor local weather alerts (KXAN, FOX 7, weather apps)

- Keep family and pets away from damaged areas

DON'T:

- Go on roof during or immediately after storm

- Touch downed power lines or standing water

- Drive through flooded areas

- Attempt DIY repairs on damaged roof

2. Stop Further Damage (If Safe)

Interior protection:

- Move furniture/valuables away from active leaks

- Place buckets, towels, or tarps under leaks

- Take photos/videos of water intrusion

- Turn off electricity to affected rooms (if flooding)

Important: Texas law requires homeowners to 'mitigate' (prevent) further damage. Insurance covers reasonable emergency repairs like tarping.

3. Initial Damage Documentation

What to photograph:

- Overall exterior views of roof from ground

- Close-ups of visible damage (if safely accessible)

- Hail on ground with size reference (quarter, golf ball)

- Damaged gutters, vents, siding, windows

- Interior water damage, stains, and soaked items

- Neighboring homes with similar damage

- Any fallen trees or branches

Pro tip: Take videos with narration describing what you see and when storm occurred. Timestamped photos are valuable evidence.

4. Contact Your Insurance Company

Call within 24-48 hours:

- File claim immediately (even if damage seems minor)

- Get claim number and adjuster assignment

- Ask about 'emergency mitigation' coverage (temporary repairs)

- Request inspection ASAP

- Ask about filing deadline (typically 1-2 years in Texas)

Information you'll need:

- Policy number

- Date and time of storm

- Brief description of damage

- Your contact information

Understanding Leander Storm Damage

Most Common Storm Threats

Hail Storms (March-May Peak)

Why Leander gets hit hard:

- Hill Country topography creates severe updrafts

- Warm, moist air from Gulf meets cold fronts

- Leander sits in prime 'Hail Alley' location

Recent major hailstorms:

- March 2024: Golf ball hail in Crystal Falls, Travisso

- April 2023: Baseball-sized hail near 183A corridor

- May 2022: Severe storms across Mason Hills

- March 2021: Widespread damage in Block House Creek area

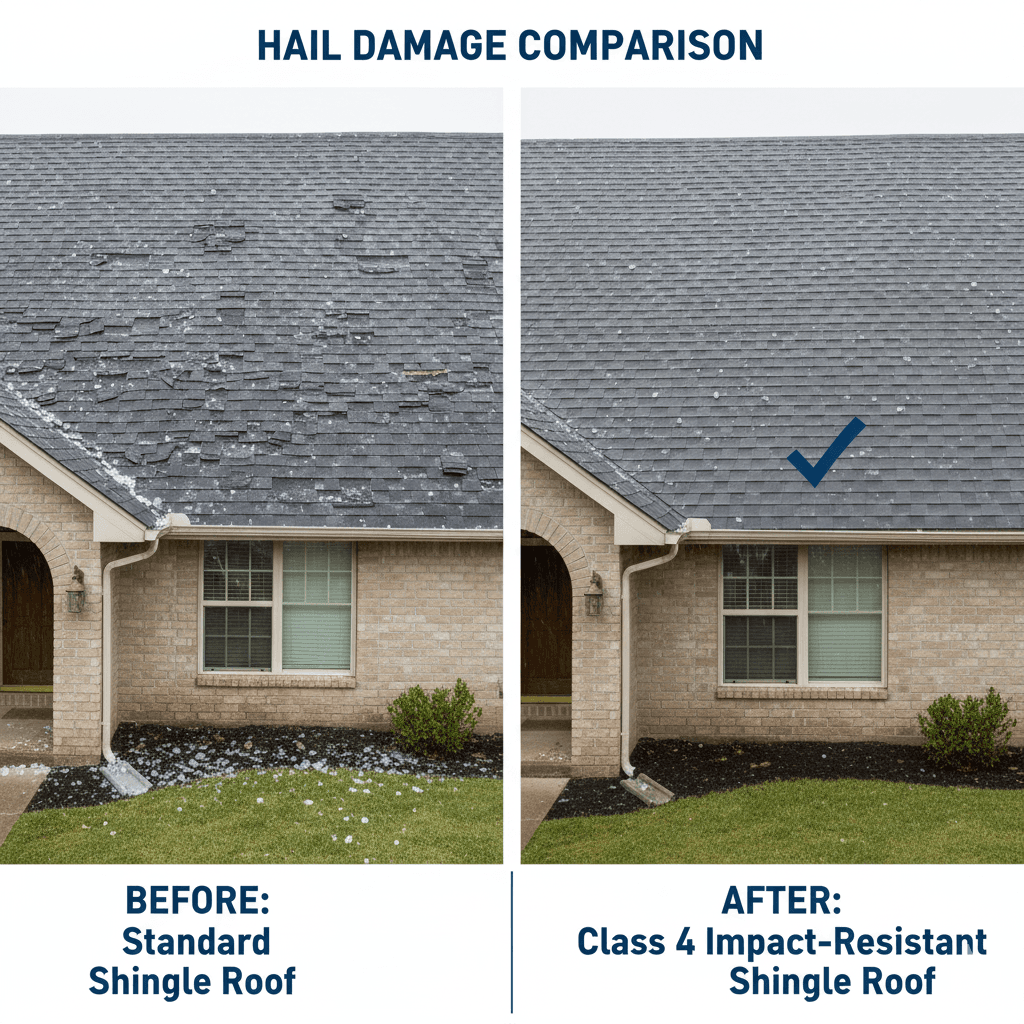

Hail damage signs:

- Shingles: Dark bruises, granule loss, cracked seal strips

- Gutters: Dents along edges and downspouts

- Vents/boots: Cracked or dented caps

- AC unit: Dented fins (check condenser)

- Siding: Impact marks, cracks, holes

- Windows: Cracked glass, broken screens

Wind Damage (Year-Round)

Leander wind threats:

- Thunderstorm straight-line winds (60-80 mph)

- Tornado activity (Leander is in moderate risk zone)

- Hill Country funneling effect increases speeds

Wind damage signs:

- Missing shingles (entire pieces gone)

- Lifted/creased shingles exposing underlayment

- Damaged flashing around chimneys and vents

- Torn gutters or downspouts

- Broken tree branches on roof

Flash Flooding (Summer Storms)

Why Leander floods:

- Rapid development with less permeable surface

- Brushy Creek and tributaries overflow quickly

- Clay soil doesn't absorb water fast

Flood-related roof damage:

- Water backing up under shingles

- Saturated insulation and decking

- Mold and mildew growth

- Structural stress from water weight

How to File a Successful Leander Insurance Claim

Step 1: Know Your Policy

Key Coverage Terms

Dwelling Coverage:

- Pays for roof repair or replacement

- Usually covers 'sudden and accidental' damage

- Storm damage almost always covered in Texas

Actual Cash Value (ACV) vs. Replacement Cost Value (RCV):

- ACV: Depreciated value (pays less initially)

- RCV: Full replacement cost (better coverage)

- Most get ACV first, RCV after work completed

Deductible:

- What you pay out of pocket

- Leander typically: $1,000-$5,000 (often 1-2% of home value)

- Cannot be legally 'waived' by contractors

Depreciation Holdback:

- Insurance holds back depreciation amount

- Released after repairs completed and inspected

- Keep all receipts and documentation

Texas-Specific Insurance Rules

✅ Insurance must respond within 15 business days

✅ Must accept or deny claim within 60 days (after agreement on value)

✅ Can reopen claim if underpaid (within policy limits)

✅ Bad faith practices are illegal (but document everything)

Step 2: Get Professional Inspection

Why this matters: Insurance adjusters work for the insurance company. Having YOUR contractor present levels the playing field.

What we provide (free):

- Comprehensive roof inspection

- Detailed damage documentation with photos

- Written assessment report

- Presence during adjuster inspection

- Insurance estimate review

- Supplement writing (additional items adjuster missed)

Red flags to avoid:

❌ Contractors who knock on your door uninvited

❌ Offers to 'waive your deductible' (insurance fraud)

❌ Requires full payment before insurance settles

❌ Out-of-state company with no local presence

❌ Pressure to sign contract immediately

Green flags to look for:

✅ Local Leander office, owner-operated

✅ CertainTeed certified contractor

✅ Licensed and insured (verify!)

✅ Strong local reviews (100+ Google reviews)

✅ Transparent process and pricing

✅ Will work with YOUR timeline

Step 3: The Adjuster Inspection

What to expect:

- Adjuster inspects roof (30-90 minutes typically)

- Takes photos, measurements, damage notes

- May use drone or ladder to access roof

- Issues preliminary estimate within 7-14 days

How to prepare:

- Have YOUR contractor present (critical!)

- Point out ALL damage you've documented

- Show photos of hail on ground (proves size)

- Show neighboring damage (establishes storm pattern)

- Be professional but firm

Common adjuster tactics:

❌ 'That's just normal wear and tear'

✅ Response: 'This happened during the [date] storm. Here's proof.'

❌ 'Your roof is too old for full replacement'

✅ Response: 'My policy has RCV coverage. Age doesn't matter if damage is storm-related.'

❌ 'We'll only pay for repair, not replacement'

✅ Response: 'Texas law requires 'matching.' Patching a 15-year-old roof won't match.'

❌ 'You need 10+ squares of damage for full replacement'

✅ Response: 'That's not in my policy. Show me where it says that.'

Step 4: Review the Insurance Estimate

What should be included:

✅ Full tear-off and disposal (all layers)

✅ Synthetic underlayment (better than felt paper)

✅ Ice & water shield (valleys, eaves, penetrations)

✅ Drip edge replacement (all edges)

✅ Proper ventilation (ridge vents, soffit vents)

✅ All flashing (chimneys, pipes, walls, valleys)

✅ Pipe boots and vent caps

✅ Starter strip and hip/ridge caps

✅ Waste/dump fees

✅ Permits (required by Leander)

Red flags in estimate:

❌ ACV payout only (demand RCV)

❌ Repair estimate for 20+ year old roof (should be replacement)

❌ Excludes code upgrades (Texas law may require)

❌ Square footage way lower than reality

❌ Missing items your contractor identified

Step 5: Challenge Lowball Estimates

When estimates are too low:

Your contractor's estimate: $15,000

Insurance estimate: $9,500

Gap: $5,500 ← This requires action

How to negotiate:

- Get multiple contractor estimates (2-3 reputable companies)

- Document missed damage (photos, detailed descriptions)

- Hire public adjuster (costs 10% but often increases payout 30-50%)

- Submit supplement request (in writing, itemized)

- Request supervisor review (if initial adjuster won't budge)

- File complaint with Texas Department of Insurance (if bad faith suspected)

Success rate: 70-80% of homeowners get additional coverage through supplements.

Step 6: Get Paid

Payment Process

Step 1: Initial ACV Check

- Replacement cost MINUS depreciation

- MINUS your deductible

- Typically arrives 7-30 days after agreement

Step 2: Complete Repairs

- Hire contractor and start work

- Keep all receipts and documentation

- Take progress photos

Step 3: Final Inspection

- Insurance verifies work completed properly

- May require photos or site visit

Step 4: RCV (Recoverable Depreciation) Check

- Insurance releases held depreciation

- Typically 7-14 days after final inspection

- Completes your payment

Payment Scenarios

Mortgage on home?

- Check made out to YOU + MORTGAGE COMPANY

- Must get mortgage company endorsement

- Can take extra 2-4 weeks

No mortgage?

- Check made out to YOU only

- Can deposit immediately

- More flexibility in process

Emergency Repairs: What to Do Right Away

24/7 Emergency Tarping Service

When you need tarping:

- Active leaks causing interior damage

- Large section of roof missing or damaged

- Holes exposing interior to elements

- Severe storms forecast before repairs possible

What to expect:

- Response within 2-4 hours in Leander

- Heavy-duty tarps installed with proper attachment

- Prevents further water intrusion

- Insurance typically reimburses $300-$800

Important: DIY tarps often cause MORE damage. Improper attachment can:

- Tear remaining shingles

- Create ice dams

- Blow off in wind, becoming projectiles

Temporary Repairs (Before Full Replacement)

What insurance covers:

- Emergency tarping

- Temporary leak patches

- Tree/debris removal (if on structure)

- Water extraction and drying

What you should do:

- Document everything (photos, receipts)

- Keep invoices for all emergency work

- Submit to insurance for reimbursement

- Don't delay—'failure to mitigate' can reduce payout

Choosing a Storm Damage Contractor in Leander

The Storm Chaser Problem

After major Leander storms, out-of-state contractors flood the area. They're easy to spot:

🚩 Warning signs:

- Knock on your door uninvited

- Pressure you to sign immediately ('deal expires today!')

- Offer to 'waive your deductible' (illegal)

- No local address or showroom

- Want full payment upfront

- Lowball estimates (40-50% below normal)

- Aggressive sales tactics

Why they're dangerous:

- Disappear after taking deposit

- Do poor-quality work

- No warranty support after they leave

- Can implicate YOU in insurance fraud

- Leave you with no recourse

How to Find Legitimate Contractors

✅ Local, established business (5+ years in Leander)

✅ Physical office you can visit

✅ CertainTeed ShingleMaster Premier or CertainTeed ShingleMaster Premier certified

✅ 100+ local Google reviews

✅ Licensed and insured (verify with TDLR)

✅ Transparent, itemized estimates

✅ Written warranties (materials + workmanship)

✅ References in your neighborhood

✅ No pressure tactics

What 'Insurance Claim Assistance' Means

Legitimate services:

✅ Free inspection and damage documentation

✅ Present during adjuster inspection

✅ Detailed estimate for comparison

✅ Write supplements for missed items

✅ Explain insurance process and terminology

✅ Review adjuster's estimate with you

Illegal practices:

❌ Offering to waive deductible

❌ Inflating damage or costs

❌ Filing false claims

❌ Accepting 'assignment of benefits' (illegal in Texas for roofing)

❌ Demanding payment before settlement

Common Leander Storm Damage Mistakes

❌ Mistake #1: Waiting Too Long

The problem:

- Hail damage accelerates (small cracks become leaks)

- Evidence disappears (hail melts, wind damage worsens)

- Statute of limitations on claims (1-2 years typically)

- Interior damage compounds

The fix: Contact insurance within 48-72 hours. Even if unsure about damage, file a claim. You can always withdraw if unnecessary.

❌ Mistake #2: Not Documenting Thoroughly

The problem: Adjusters only cover what they see. If you don't show damage, it won't be included in estimate.

The fix: Take 50-100 photos:

- Roof from all angles

- Close-ups of every damaged shingle

- Gutters, vents, flashing

- Interior stains

- Neighboring damage

- Hail on ground with size reference

❌ Mistake #3: Accepting First Offer

The problem: Initial adjuster estimates are often 20-40% low. They're incentivized to minimize payouts.

The fix: Get independent contractor estimates. Submit supplements. Challenge lowball offers. Most insurers negotiate.

❌ Mistake #4: Hiring First Contractor Who Knocks

The problem: Storm chasers disappear with deposits. Poor work. Fraud risk. No warranty support.

The fix: Get 3+ estimates from LOCAL, CERTIFIED contractors. Check reviews. Verify insurance. Visit their office.

❌ Mistake #5: Starting Work Before Approval

The problem: If you complete repairs before adjuster inspects, they'll question storm causation. Contract signed before settlement = you're liable for full cost regardless.

The fix: Emergency tarps OK (and recommended). Full replacement waits for approval—unless you're paying cash.

❌ Mistake #6: Not Understanding Your Policy

The problem: Not knowing your coverage means accepting less than you deserve.

The fix: Read your policy. Ask questions. Understand:

- ACV vs RCV

- Deductible amount

- Coverage limits

- Exclusions

- Code upgrade coverage

Leander Storm Damage Cost Guide

Emergency Services

| Service | Typical Cost | Insurance Coverage |

|---|---|---|

| Emergency tarp (24hr) | $300-$800 | Usually covered |

| Minor leak patch | $150-$400 | Usually covered |

| Tree removal (on house) | $500-$3,000 | Covered if storm-caused |

| Water extraction/drying | $500-$2,000 | Covered (prevents further damage) |

Full Restoration

| Damage Type | Repair Cost | Replacement Cost | Insurance Covers? |

|---|---|---|---|

| Minor hail (5-10 squares) | $2,500-$5,000 | $10,000-$16,000 | Usually full replacement |

| Moderate hail (10-20 squares) | N/A (too extensive) | $12,000-$18,000 | Yes |

| Severe hail (full roof) | N/A | $14,000-$25,000+ | Yes |

| Wind (missing shingles) | $1,500-$6,000 | $10,000-$20,000 | If widespread, yes |

| Water damage (interior) | $2,000-$15,000 | N/A | If storm-caused, yes |

Average Leander storm claim: $14,000-$18,000 (full roof replacement)

Average deductible: $1,500-$3,000 (1-2% of home value)

Average out-of-pocket: $2,000-$4,000 (deductible + upgrades)

After a Major Leander Storm: What to Expect

Typical Timeline

Day 0 (Storm Day):

- Hail/wind event occurs

- Homeowners assess obvious damage

- Emergency contractors swamped with calls

Days 1-3:

- Insurance claims filed (hundreds in Leander)

- Professional inspections scheduled

- Storm chasers arrive

- Social media fills with damage reports

Week 1:

- Insurance adjusters schedule inspections

- Contractors write estimates

- Tarps installed on damaged homes

- Material shortages begin

Weeks 2-4:

- Adjuster inspections complete

- Initial estimates issued

- Supplement negotiations

- Approved projects begin

Months 2-6:

- Peak repair season

- Material lead times extend (4-8 weeks)

- Final inspections and RCV payments

- Late claimants rush to file

Material Shortages After Major Storms

What happens:

- Sudden demand overwhelms supply

- Popular shingle colors out of stock

- Lead times extend from days to months

- Prices may increase temporarily

Pro tip: File claims early. Get in line with contractors ASAP. Accept slight color variations if necessary to avoid 6-month delays.

Leander Neighborhoods and Storm Risk

Crystal Falls

Risk level: High

Why: Open terrain, elevation changes

Common damage: Hail, wind-driven rain

Mason Hills

Risk level: Moderate-High

Why: Hill Country edge location

Common damage: Hail, wind

Summerlyn

Risk level: Moderate

Why: Newer construction, better drainage

Common damage: Hail primarily

Travisso

Risk level: Moderate-High

Why: Exposed location near 183A

Common damage: Hail, wind

San Gabriel Village/Block House Creek

Risk level: Moderate

Why: Mature trees (falling branches)

Common damage: Wind, tree damage

Your Leander Storm Damage Experts

Don't navigate insurance claims alone. Ripple Roofing & Construction helps Leander families recover from storm damage with:

✅ Local Leander Expertise (we know the area)

✅ CertainTeed ShingleMaster Premier Certified (top-tier contractor)

✅ 5.0/5 Star Reviews on Google

✅ Free Storm Damage Inspections (no obligation)

✅ We Meet Your Adjuster (advocate for you)

✅ 24/7 Emergency Service (tarps, emergency repairs)

✅ Lifetime Workmanship Warranty

What We Do for Leander Homeowners:

- Free inspection within 24-48 hours

- Detailed damage documentation with photos

- Attend adjuster meeting (we're YOUR advocate)

- Review insurance estimate line by line

- Write supplements for missed items

- Handle all permits and code requirements

- Complete quality repairs with warranty

- Final inspection coordination for RCV payment

Serving All Leander Neighborhoods:

Crystal Falls • Mason Hills • Summerlyn • San Gabriel Village • Block House Creek • Northline • Palmera Ridge • Travisso • and all surrounding areas

Get Help Now - 24/7 Emergency Service

Storm damage? Don't wait. Every hour increases interior damage risk.

Call (512) 763-5277 for immediate assistance

Or request free inspection online

Available 24/7 for Leander emergency roofing services.

About the Author: Jonathan helps Leander families navigate insurance claims and recover from storm damage. Ripple Roofing & Construction is CertainTeed ShingleMaster Premier certified and serves the Leander community from its Round Rock headquarters.